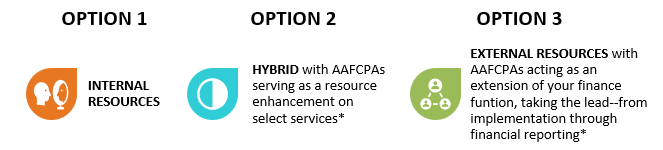

Implementing the new lease standard is not just a one-time exercise. It requires changes to accounting processes and financial reporting controls. Accounting policy elections and practical expedients will affect the overall process and timeline—so AAFCPAs advises clients to assess them early. Effective implementation requires a thorough evaluation of resources and your organization should identify someone to take the lead for this work.

Many chief finance executives expect the level of effort to implement to be extremely painful.

Key Considerations

Define a lease

Exceptions

What is included in cost of right of use assets

Types of leases

Capitalized operating leases

Finance leases

Financial statement impact

Transition issues

Guidance for new leases

Tax considerations

GAAP vs. other basis of accounting

Lessor accounting

AAFCPAs Lease ASU Implementation Checklist

AAFCPAs designed a comprehensive checklist to help clients understand the scope of the ASU implementation process.

Assessing the impact of the standard on the organization/company, including assisting with the inventorying of all existing leases and terms; assisting with the development of an implementation schedule to appropriately allocate internal resources to achieve compliance with the new standard; reviewing and updating accounting policies and procedures to reflect the required changes.

Analysis of qualifying lease agreements, including any lease modifications and documentation of detailed summaries and accounting treatments; guidance on interpreting the criteria necessary to classify leases as operation or financing; guidance on bundling lease agreements and similar polices and accounting treatments with the goal of improving efficiency of analysis; and assessing the impact and desirability of electing available practical expedients.

Assessing the impact of the new standard on debt covenants.

Assessing the impact on drafting financial statements, footnote disclosures, including transition election and presentation.

Lease Accounting Software Selection & Implementation: AAFCPAs will identify the most appropriate IT solutions, including a cost/benefit analysis related to the utilization of lease software solutions and system selection including implementation support.

AAFCPAs assembled its Lease Accounting Task Force to ensure clients can implement the new ASU with efficiency and ease. We have been dedicated to interpreting and advising clients on the ASU since introduced by the FASB back in 2016.

Contact us to discuss how the new lease standard will impact your organization—and how we can help.

Jeffrey is a Partner in the Commercial Assurance Division at AAFCPAs, where he provides technical accounting advisory solutions and concurring partner reviews. This includes guidance on standards implementation and interpretation. He is a leader of the firm’s Accounting and Assurance (A&A) Committee, Revenue Recognition and Lease Accounting Task Forces, as well as AAFCPAs’ Risk Committee.

Jeffrey brings empathy, patience, respect, and the will to inspire into his work as coach and mentor for the company’s pioneering …

Matt leads AAFCPAs’ Healthcare Division, providing assurance, tax and advisory solutions for sophisticated and complex healthcare organizations including Federally Qualified Health Centers, behavioral health providers, home care agencies and hospices, nursing homes, and senior care living centers. Matt advises healthcare providers on consolidation and coordination of care, including the integration of behavioral health into the primary care delivery system. He also provides consulting solutions for providers transitioning to new value-based reimbursement models, and data driven …

0

We use cookies to ensure we give you the best experience on our website. By continuing your visit, you consent to the use of these cookies. See our:

Functional cookies

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

We use cookies to optimize our website and our service.

Functional cookies

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.