States Not Adopting Federal Due Date Change for C Corporations

Posted on

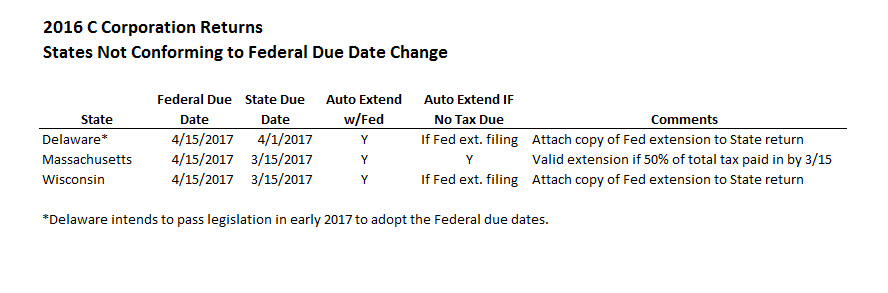

Please be aware, the IRS changed the due date for filing calendar year C corporation returns from 3/15 to 4/15 (or the 15th day of the fourth month following the close of the corporation’s fiscal year). Although most states have adjusted their statutes or administrative rulings to accommodate the Federal change, there are three states (Massachusetts, Delaware, and Wisconsin) whose due dates now fall before the new Federal due date.

AAFCPAs has provided the below chart for your convenience, which outlines additional detail regarding the process for filing extensions in these states, including whether a Federal extension will automatically act as a valid state extension so long as all taxes are properly paid in by the state due date.

AAFCPAs encourages clients to take note of these nuances when planning to file corporate extensions. While the above chart highlights those limited situations where the state due date precedes the Federal due date, there are other things to consider:

States whose C corporation filing date has traditionally fallen after the Federal due date might not have changed their statute. For example, New Jersey’s due date remains April 15, while Connecticut moved their date from April 1 to May 1.

A number of states have accelerated their partnership filing dates from April 15 to March 15 to be consistent with the change in the Federal due date.

If you have any questions about tax planning or compliance, please contact your AAFCPAs partner or Richard Weiner at 774.512.4078 or rweiner@nullaafcpa.com.

Rich brings more than 35 years of tax experience to privately held and publicly traded companies across the United States and internationally. He advises growth-oriented businesses navigating complex tax environments, offering practical guidance grounded in industry knowledge spanning software, biotechnology, medical device, life sciences, manufacturing, retail, professional services, and publishing.

Business leaders engage Rich to connect tax planning with broader operational and financial goals. Working alongside executive and finance teams, he identifies opportunities to streamline operations, …

0

We use cookies to ensure we give you the best experience on our website. By continuing your visit, you consent to the use of these cookies. See our:

Functional cookies

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

We use cookies to optimize our website and our service.

Functional cookies

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.