GASB Issues Statement 103: What Government Entities Need to Know

The Government Accounting Standards Board (GASB) has issued Statement 103, Financial Reporting Model Improvements, introducing meaningful changes to how government entities present their financial information. With an effective date for fiscal years beginning after June 15, 2025 (for June 30, 2026 year-ends), organizations should begin preparing now.

Why These Changes Matter

GASB 103 represents a broad effort to improve the clarity, comparability, and usefulness of government financial statements. The updates affect several core areas, including Management’s Discussion and Analysis (MD&A), the reporting of unusual or infrequent items, profit and loss presentation, and budgetary comparison information.

Collectively, these changes address long‑standing challenges in government financial reporting by clarifying what belongs in each section of the financial statements and by promoting more consistent presentation across government entities.

Management’s Discussion and Analysis

MD&A receives significant attention under GASB 103, with clearer direction on required content and items that should be excluded. The updated guidance identifies five required components:

- An overview of the financial statements

- A financial summary highlighting key results

- Detailed analysis of significant financial activities

- Discussion of significant capital asset and long‑term financing activity, including major additions, disposals, policy changes, and debt‑related activity such as leases and subscription‑based IT arrangements (SBITAs)

- A discussion of currently known facts, decisions, or conditions that may affect future financial position

GASB 103 also removes budget‑to‑actual analysis from MD&A. That information is now presented separately as Required Supplementary Information (RSI), as required for the general fund and each major special revenue fund that has a legally adopted annual budget.

Unusual or Infrequent Items

GASB 103 also provides clearer guidance on the reporting of unusual or infrequent items. To qualify, events must meet the criteria established in GASB 62, Codification of Accounting and Financial Reporting Guidance Contained in Pre-November 30, 1989 FASB and AICPA Pronouncements, meaning they must be both unusual in nature and infrequent in occurrence.

Related inflows and outflows must be reported separately as the final flows of resources before the net change in resources in government‑wide, governmental fund, and proprietary fund statements of resource flows.

Updated Proprietary Fund Nonoperating Revenue and Expense Definitions

To improve comparability across governments, GASB 103 introduces updated definitions for proprietary fund nonoperating revenues and expenses. Under the new guidance, nonoperating items include:

- Subsidies received and provided

- Contributions to permanent and term endowments

- Revenues and expenses related to financing

- Resources from the disposal of capital assets and inventory

- Investment income and expenses

The standard includes a more detailed discussion of subsidies, focusing on the absence of an exchange of goods or services and the effect on pricing policies. GASB 103 intentionally avoids bright‑line tests for determining principal operations, placing greater emphasis on professional judgment.

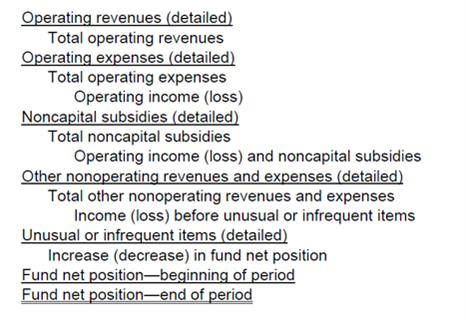

Illustrative Example Provided in GASB 103

GASB 103 provides the following illustrative presentation for a proprietary fund statement of revenues, expenses, and changes in fund net position:

Budgetary Comparison Information Changes

GASB 103 requires budgetary comparison schedules to be presented as RSI for the general fund and each major special revenue fund with a legally adopted annual budget. These schedules must include separate columns showing:

- Variances between original and final budget amounts

- Variances between final budget amounts and actual results

Governments must also explain significant variances in the notes to the RSI, increasing transparency around budget performance.

Preparing for Implementation

With the effective date approaching, AAFCPAs advises that clients begin evaluating how these changes will affect their financial reporting processes and timelines. Early planning can help ensure smoother implementation.

How We Help

AAFCPAs works closely with education organizations—ranging from independent and charter schools to colleges, universities, and charter management organizations—to help them navigate complex financial reporting and regulatory requirements with confidence. Our Education Practice understands the funding models, governance structures, and compliance pressures unique to education institutions, including the practical implications of evolving accounting standards such as GASB 103. We support finance teams and leadership as they assess how new guidance affects financial presentation, management discussion and analysis, and budgetary reporting, while maintaining clear and consistent communication with boards, bondholders, regulators, and other stakeholders.

Beyond technical accounting advisory, we help schools strengthen financial oversight through outsourced accounting and financial leadership, evaluate the accounting and reporting implications of capital campaigns and debt structures, design controls and reporting processes for endowments and alternative investments, and align fundraising activities with compliance and donor expectations. Whether an institution is undertaking new initiatives, expanding programs, or preparing for heightened scrutiny through audits or accreditation reviews, AAFCPAs brings deep education‑industry insight and practical judgment to ensure financial reporting supports transparency, long‑term sustainability, and informed decision‑making.

These insights were contributed by Nichole A. Reilly, CPA, MBA, Partner.

Questions? Reach out to our author directly or your AAFCPAs partner.

AAFCPAs offers a wealth of resources on accounting standards. Subscribe to get alerts and insights in your inbox.

About the Author